Scenario Says

Those demanding we limit our options to renewable-energy-only have tacitly diminished the bulk of AEMO’s Integrated System Plan.

To briefly remind ourselves about what the ISP is, the Australian Energy Council wrote:

Recommendation 5.1 of the Finkel Review was for AEMO to prepare an ISP “to facilitate the efficient development and connection of renewable energy zones across the National Electricity Market”. The ISP effectively replaces the National Transmission Network Development Plan (NTNDP) which performed a similar, “independent, strategic view of the efficient development of the NEM transmission grid over a 20-year planning horizon”. Unlike the restricted focus of state-based transmission planners, the ISP (as the NTNDP did before it) seeks to assess the NEM’s needs holistically.

The ISP considers the power system’s transition as a result of coal-fired generation retiring, the construction of new renewable generation, and changes in operational demand as a result of economic conditions, energy efficiency and distributed energy resource penetration.

The Central scenario of the recently released 2020 update features 8.5 gigawatts of brown and black coal capacity persisting on the NEM after 2040. All alternative scenarios but one give a similar result.

The ISP report provides a snapshot week of the modelling in 2035 to illustrate this:

This is with high modelled solar and wind output serving most of demand & charging up vast new storage capacity… underpinned by gigawatts of coal. What if 15 years of inclusive low-emission policy ambition replaced all the coal?

After all, we’re already talking about a long planning horizon, considerable market intervention and many billions of dollars.

And so, the championing of the Step Change scenario which shrinks coal to practically nil by the mid-2030s. If you’re still betting against nuclear energy, it’s naturally going to be your preference.

But contrary to assurances, the challenge does come in building so much new wind and solar, as well as the rest of the non-generating infrastructure (hypothetically) necessary to make it work in real life like it does in the spreadsheets. It’s a monumental task that deserves no credulity.

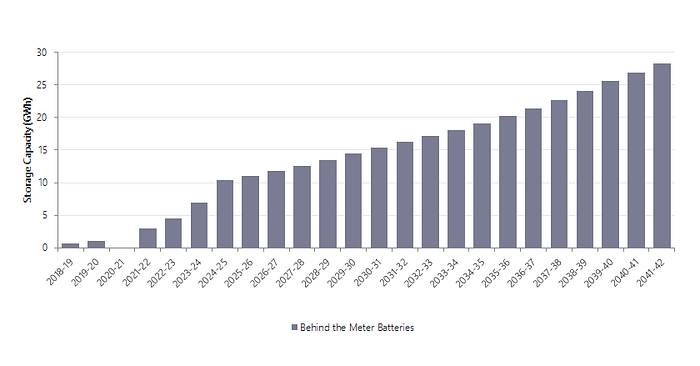

To focus on a single aspect of this infrastructure: distributed battery storage. This is how much gigawatt hour energy capacity addition is modelled in the Step Change scenario:

The first thing to note is that this is just a fraction of the necessary storage. For a little bit of perspective, the IEA put all global battery capacity at 7 GWh in 2018.

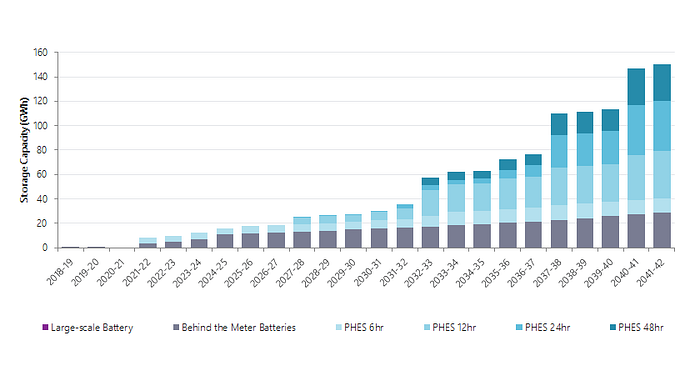

Here’s all the grid-scale batteries and pumped hydro projects:

But this excludes Snowy 2.0, as some would prefer.

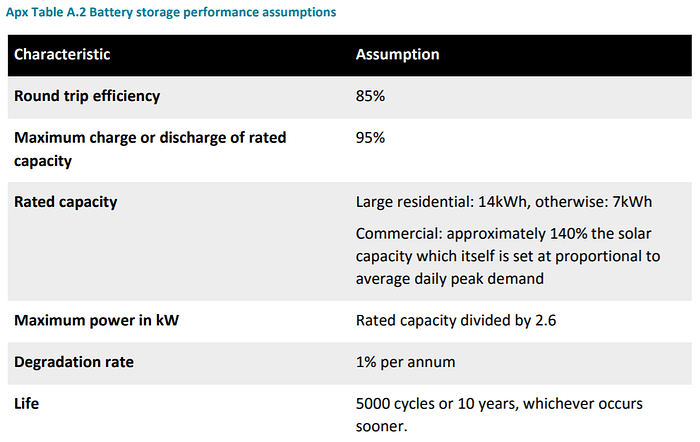

But back to those batteries. Those distributed battery storage systems which the supporting work by the CSIRO assumes will last a single decade:

The last five years have already showed us what battery over-confidence looks like, as observed at WattClarity:

While home battery installations increased year on year until 2018, there was no increase in 2019. If installations level off at this rate, we won’t have Morgan Stanley’s mid-range estimate of one million installations until 2060. The zero increase was despite South Australia’s massive battery subsidy of up to $6,000 being in full swing throughout 2019. Without the subsidy, installations last year presumably would have been several thousand less, and installation numbers would be going backwards.

Just for the sake of comparison, if the Step Change scenario’s 51.22 GWh of batteries by 2040 were comprised of a market leading 14 kWh class home storage system, it would equal almost 3.66 million installations.

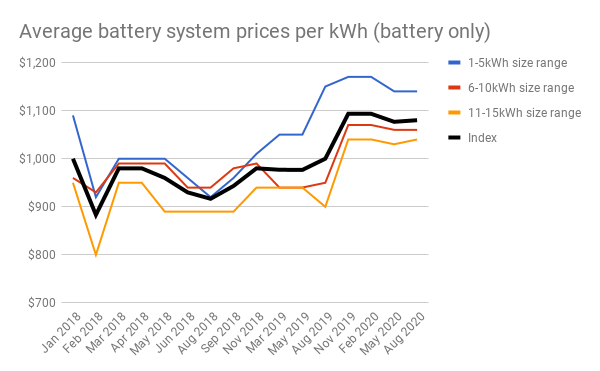

Furthermore, we’re yet to witness the price drop for consumers that was a fundamental underpinning of this confidence.

But most problematic is the issue of emissions. The commentary applauds AEMO’s low projected NEM emissions intensity — which will be lower than even France’s!

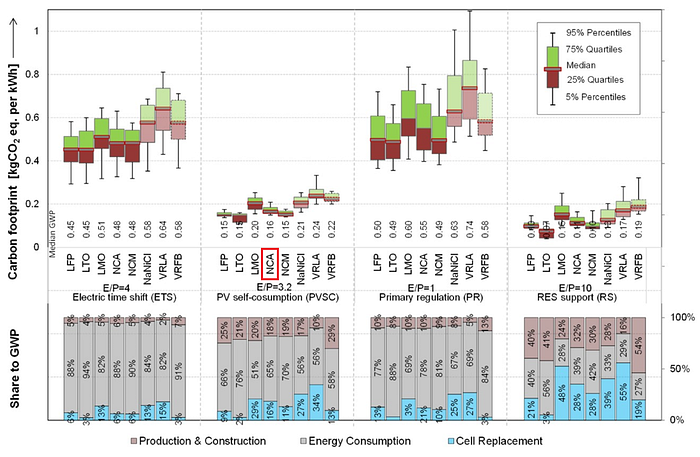

As observed previously, AEMO accounts for operational rather than life cycle emissions. While all that rooftop solar has a very low life cycle footprint, it isn’t zero. Adding battery storage actually increases it. There still isn’t as much scholarship on this as there should be but a study from 2016 looked at the footprint of PV self-consumption for various battery options (mostly lithium ion) on a 20 year basis, cycling once per day and accounting for unit replacement:

This work concluded that adding battery storage based on NCA chemistry (which is used by the dominant brand in Australia) to rooftop PV results in median emissions of 160 gCO₂e/kWh.

Obviously this sort of result can change with product efficiencies over time as well as starting assumptions. But if comparisons are going to be drawn with the real life success we see in other countries today, more of this literature must be consulted, not neglected.

I’ve been communicating on AEMO’s ISP process for Bright New World for a couple of years now. We’ll keep engaging and analysing the valuable material. Readers are naturally encouraged to consult the ISP report for themselves, as well… especially when other commentary gets suspiciously selective.

Oscar Archer holds a PhD in chemistry and has been analysing energy issues for over 15 years, focusing on nuclear technology for six, with a background in manufacturing and QA. He helps out at Adelaide-based Bright New World as Senior Advisor (we want your support!)and writes for The Fourth Generation. Find him @OskaArcher on Twitter.